Page 69 - Housing Solutions Annual Report

P. 69

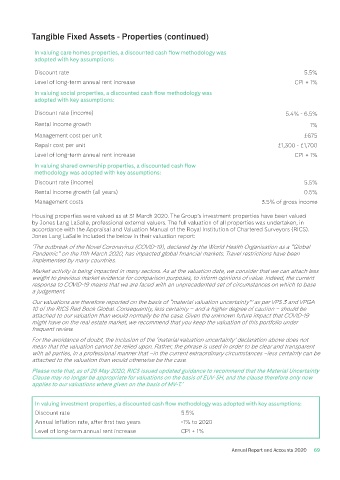

Tangible Fixed Assets - Properties (continued)

In valuing care homes properties, a discounted cash flow methodology was

adopted with key assumptions:

Discount rate 5.5%

Level of long-term annual rent increase CPI + 1%

In valuing social properties, a discounted cash flow methodology was

adopted with key assumptions:

Discount rate (income) 5.4% - 6.5%

Rental income growth 1%

Management cost per unit £675

Repair cost per unit £1,300 - £1,700

Level of long-term annual rent increase CPI + 1%

In valuing shared ownership properties, a discounted cash flow

methodology was adopted with key assumptions:

Discount rate (income) 5.5%

Rental income growth (all years) 0.5%

Management costs 3.5% of gross income

Housing properties were valued as at 31 March 2020. The Group’s investment properties have been valued

by Jones Lang LaSalle, professional external valuers. The full valuation of all properties was undertaken, in

accordance with the Appraisal and Valuation Manual of the Royal Institution of Chartered Surveyors (RICS).

Jones Lang LaSalle included the below in their valuation report:

‘The outbreak of the Novel Coronavirus (COVID-19), declared by the World Health Organisation as a “Global

Pandemic” on the 11th March 2020, has impacted global financial markets. Travel restrictions have been

implemented by many countries.

Market activity is being impacted in many sectors. As at the valuation date, we consider that we can attach less

weight to previous market evidence for comparison purposes, to inform opinions of value. Indeed, the current

response to COVID-19 means that we are faced with an unprecedented set of circumstances on which to base

a judgement.

Our valuations are therefore reported on the basis of “material valuation uncertainty”’ as per VPS 3 and VPGA

10 of the RICS Red Book Global. Consequently, less certainty – and a higher degree of caution – should be

attached to our valuation than would normally be the case. Given the unknown future impact that COVID-19

might have on the real estate market, we recommend that you keep the valuation of this portfolio under

frequent review.

For the avoidance of doubt, the inclusion of the ‘material valuation uncertainty’ declaration above does not

mean that the valuation cannot be relied upon. Rather, the phrase is used in order to be clear and transparent

with all parties, in a professional manner that –in the current extraordinary circumstances –less certainty can be

attached to the valuation than would otherwise be the case.

Please note that, as of 26 May 2020, RICS issued updated guidance to recommend that the Material Uncertainty

Clause may no longer be appropriate for valuations on the basis of EUV-SH, and the clause therefore only now

applies to our valuations where given on the basis of MV-T.’

In valuing investment properties, a discounted cash flow methodology was adopted with key assumptions:

Discount rate 5.5%

Annual inflation rate, after first two years -1% to 2020

Level of long-term annual rent increase CPI + 1%

Annual Report and Accounts 2020 69

10/11/2020 13:35

16645.02 HS Annual Report 86pp A4 v10.indd 69 10/11/2020 13:35

16645.02 HS Annual Report 86pp A4 v10.indd 69